Mid‑Market Canadian Financings & Transactions – April 2026

April 2026 Canadian Mid-Market M&A and Financing Report | Key Deals, Trends & Analysis

Comprehensive analysis of Canadian mid-market M&A, financings, acquisitions, critical minerals, private placements, and strategic transactions announced in April 2026. Includes major deals, market trends, valuation insights, and sector analysis.

April 2026 Mid-Market Deals: Executive Summary

April 2026 was an unusually active month for Canadian mid-market dealmaking, but the activity was highly concentrated. The upper end of the in-scope range was defined by a handful of large, strategically significant transactions.

The dominant April theme was mining, critical minerals, and resource-linked capital. Most identified, disclosed-size mid-market transactions were either mining financings, streams/royalties, or M&A involving exploration and development assets, including NMG, New Found Gold, Fireweed, Abitibi, Selkirk, Gold Candle/Fokus, OR Royalties/Canadian Copper, and Versamet/Eskay.

In other words, Canada’s April mid-market was not broad-based in sector terms; it was resource-heavy and capital-intensive.

Capital structure patterns were equally distinctive.

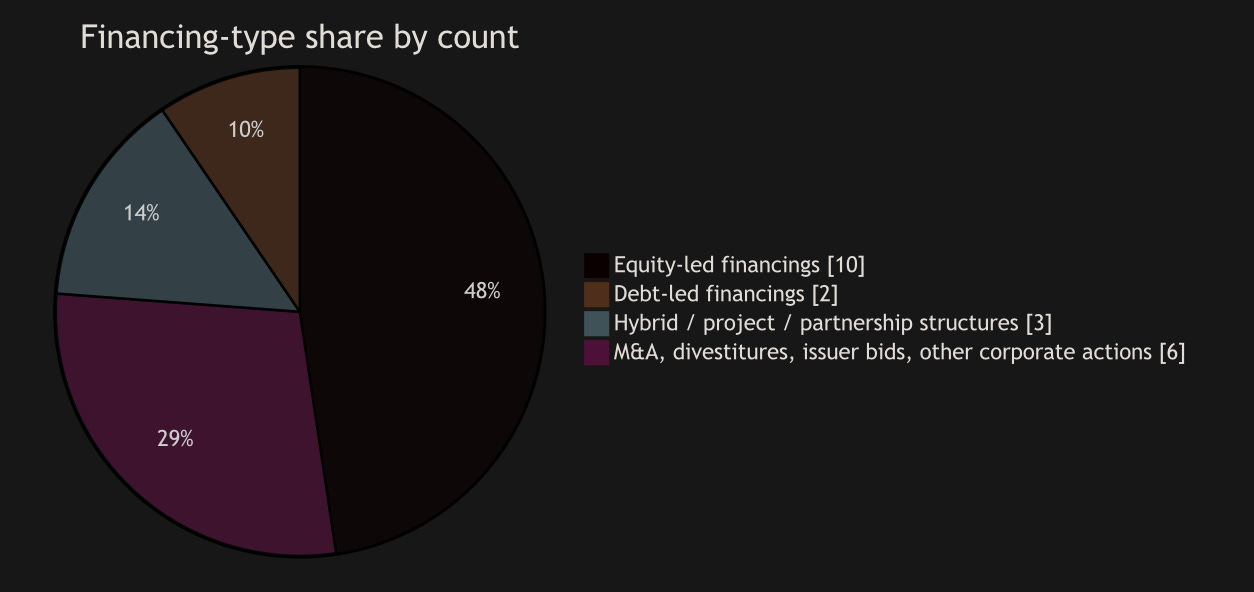

Equity-led financings dominated by count, especially in exploration and development stories.

Debt appeared selectively and mostly in refinancings or hybrid packages, such as Extendicare’s unsecured note issuance.

Strategic and quasi-sovereign capital was also unusually visible, with Canada Growth Fund, Investissement Québec, Eni, JX Advanced Metals, Discovery Silver, BMI Group, EdgePoint, and Hartree all appearing as cornerstone or strategic counterparties.

Valuation multiples were the exception, not the rule. Most April deals involved exploration companies, project financings, streaming structures, or capital returns rather than mature cash-flowing businesses, so EV/EBITDA and P/S disclosures were usually absent.

The clearest directly inferable multiple in the April set came from Lightspeed’s Upserve divestiture: the up-to-U.S.$81 million consideration against roughly U.S.$140 million of revenue on the divested operations implies up to roughly 0.6x revenue, or about 0.3x on the fixed-cash portion alone (source).

For context, April also included several Canada-related mega-deals that were outside the mid-market band and are therefore excluded from the core dataset below, including Shell/ARC, Eldorado/Foran, and Blackline Safety’s take-private (source).

Scope and methodology

This report uses a practical “occurred in April 2026” filter: deals were included if they were announced, completed, or had a material step-change in April 2026.

“Mid-market” is applied as requested: enterprise value or financing size between C$10 million and C$500 million, using company-disclosed currency where available and an approximate working U.S.$/C$ conversion only for the purpose of ranking mixed-currency transactions inside the report. If a materially relevant April Canada-related transaction had undisclosed value, it is shown separately.

The financing-type mix by deal count shows why April felt more like a structuring market than a pure M&A market. Straight equity deals dominated, but hybrid packages and corporate actions still accounted for a large minority of activity.

The valuation pattern is just as important as the count pattern. April’s disclosed-value core set did not produce a deep bench of EBITDA multiples because the flow was dominated by exploration equity, project capital, streams, and capital-structure actions. The practical implication is that April valuation work mostly turned on premiums, ownership stakes, milestone conditions, warrant economics, and capital-stack ranking, not on conventional EV/EBITDA.

Top Ten April 2026 Mid-Market Deals

The ranking below uses headline disclosed values and a rough U.S.$/C$ normalization only where needed. At the bottom end of the top ten, the ranking is sensitive to FX assumptions; ACT and Gold Candle were effectively a near-tie on that basis.

Versamet / Eskay Creek stream. Versamet’s U.S.$360 million acquisition of the 3.52% Eskay Creek gold stream was the clearest April example of an asset-level financing/acquisition hybrid sitting just inside the mid-market cap.

Strategically, it converted a Canadian precious-metals construction asset into a tradable, leveraged royalty-style growth engine for the buyer. Structurally, it was notable for the amended U.S.$400 million facility, the uncapped life-of-mine stream, the 10% ongoing delivery payment, and the step-up mechanism if project completion tests slipped. It is a reminder that April’s biggest “mid-market” transactions were often not classic corporate takeovers, but carefully engineered stream-plus-credit deals (source).

Agnico Eagle / Aurion. The Aurion transaction shows how strategic buyers treated high-quality exploration optionality in April. The headline value was about C$481 million, with no financing condition highlighted in the issuer release. Governance and process were central: Aurion’s special committee retained Haywood, the board received support from Stifel, and the deal required not only two-thirds shareholder approval but also MI 61-101 majority-of-minority approval and court clearance (source). This might be less about conventional operating multiples and more about premium, certainty, and governance hygiene in a strategic public-company takeout.

Extendicare senior unsecured notes. Extendicare’s C$450 million inaugural investment-grade bond issue stands out because it was one of the month’s few large debt-led deals outside mining. The company used the proceeds mainly to refinance and re-rank existing debt, turning the residual revolver into senior unsecured debt pari passu with the new notes (source).

For investors, the significance was not just issuance size, but the migration to an investment-grade-style balance sheet architecture. For advisors, it demonstrated that April debt capital was available for issuers with stable underlying cash flows even while risk capital remained resource-biased elsewhere in the market.

NMG Phase-2 Matawinie package. NMG’s April financing package was one of the month’s highest-quality examples of stacked capital: industrial capital from Eni, quasi-sovereign/government capital from Canada Growth Fund and Investissement Québec, and a public subscription-receipt offering underwritten by BMO and National Bank.

The public leg closed at roughly U.S.$96.5 million after full over-allotment exercise, and the strategic private placement was framed at approximately U.S.$213 million, subject to shareholder and exchange approvals.

The package also sat on top of previously announced U.S.$335 million debt commitments. That is classic late-stage Canadian critical-minerals financing: strategic anchor capital first, public equity second, project debt already lined up in the background (source).

New Found Gold finance package. New Found’s C$205 million package was arguably the cleanest April example of equity and debt being used together to advance development while preserving optionality. The debt side carried real cost: 8.75% fixed interest, 2% OID, 1% establishment fees, and warrant economics for the lender. But that pricing also shows where credit was actually clearing for development-stage Canadian resource stories (source).

The paired structure reduced sole reliance on equity dilution and created staged optionality through the second debt tranche. For investors, this might be the kind of April structure that separates “fully funded” from “cheaply funded.”

Altus Group substantial issuer bid. Altus’s C$200 million SIB is easy to overlook in a month dominated by resource financings, but it is analytically important. It captures a different side of the mid-market: capital return rather than capital raising.

The deal used cash on hand, relied on a modified Dutch auction, and required OSC exemptive relief around bid mechanics (source).

For boards and advisors, the lesson could be that even in an issuance-heavy month, issuers with balance-sheet flexibility were still willing to take advantage of perceived valuation dislocations through structured repurchases.

Rock Tech / BMI Red Rock partnership. Rock Tech’s announced C$200 million anchor partnership with BMI Group deserves outsized attention because it was not a standard equity raise. The proposed GP/LP structure lets Rock Tech retain operational control while BMI anchors the project capital.

The up-to-C$30 million initial non-dilutive funding layer, expected to be partially matched by government programs, is especially significant. It shows how Canadian industrial and critical-minerals projects are moving toward infrastructure-style capital structures, where sponsor skill, strategic LP capital, and government matching can coexist (source).

Blue Moon Metals offerings. Blue Moon paired April final-investment-decision messaging with C$150 million of concurrent bought-deal equity offerings. The company also pointed to existing undrawn project finance under a previously announced U.S.$140 million package, effectively telling the market that the remaining construction funding plan was already mostly architected (source).

This is the kind of disclosure package that tends to attract capital even without conventional operating multiples, because the public market is really underwriting construction-readiness and capital-stack credibility rather than current earnings.

Lightspeed / Upserve divestiture. Lightspeed’s sale of the Upserve U.S. hospitality line to Skyview for up to U.S.$81 million was the clearest non-resource strategic optimization trade in the April set.

The fixed-cash portion was U.S.$44 million, with U.S.$20 million payable at closing and most of the rest within 90 days; the additional U.S.$37 million is an earnout over 24 months.

Because the divested operations contributed around U.S.$140 million in revenue, the headline consideration implies a sub-1x revenue multiple. That matters. It suggests that in April 2026, Canadian public-market-adjacent software carve-outs were being priced more conservatively than strategic resource optionality (source).

ACT / SB Directional Services. ACT’s U.S.$47 million acquisition of SB Directional Services rounds out the upper tier. The transaction is important as a mid-market energy-services consolidation marker in a month that otherwise tilted sharply to mining and capital markets.

Near-miss transactions just below that top-ten cut line included Gold Candle/Fokus at about C$63 million, Fireweed’s C$61.46 million strategic private placement, and Coelacanth’s C$60 million bought deal. Their proximity to the cut line underscores how quickly April’s “largest ten” compresses once the top four to five deals are stripped out.

Implications and outlook

For advisors, April’s message was straightforward: the Canadian mid-market was rewarding capital-stack engineering at least as much as simple origination. The most relevant advisory work was not only sell-side or buy-side M&A. It was hybrid structuring, strategic-cornerstone coordination, rights agreements, warrant economics, subscription-receipt execution, stream/royalty overlays, issuer-bid mechanics, and staged approval pathways. The April winners were the advisors that could combine corporate finance, securities, mining/project finance, and regulatory process design in one package.

For investors, April reinforced three points. First, scarce strategic assets in mining and critical minerals still drew capital even when many structures were dilutive. Second, debt remained available, but it was selective and not cheap, as New Found’s facility economics make clear. Third, where issuers could frame a transaction as simplification or sharpened focus rather than distress, markets seemed willing to tolerate aggressive structure, whether that meant capital returns at Altus or portfolio pruning at Lightspeed.

The short-term outlook into May and early June 2026 looked constructive on the evidence already visible by May 2. Several April-signed transactions were still moving through closing mechanics or later legs, including Aurion, NMG’s strategic private placement, Coelacanth, and the final close of Queen’s Road’s placement. If those transactions are a guide, the near-term pipeline likely remains mining-heavy, with continued reliance on strategic and quasi-sovereign capital, and with exchange and securities approvals remaining the main closing gatekeepers. In contrast, traditional EBITDA-multiple M&A looked less central in April’s mid-market than project-backed financings, royalty/stream deals, and portfolio simplification trades.

Open questions and limitations

A few limitations materially affect interpretation.

Some April transactions had better public disclosure than others. A few transactions were announced in April but closed in May or later, including Queen’s Road, Coelacanth, NMG’s strategic private placement, and Aurion. They remain important to the April picture because April was when the market absorbed and priced the structures, even if all cash did not settle in the month.

Finally, this is a public-announcement dataset, not a proprietary database extraction. Canada almost certainly saw additional private sponsor, family-office, lender, and bilateral mid-market activity in April 2026 that was not publicly disclosed in enough detail to be included rigorously here.

April 2026 Mid Market Deals - Conclusion

April 2026 demonstrated that the Canadian mid-market is no longer simply a domestic M&A ecosystem — it is increasingly functioning as a strategic capital formation engine for globally important industries.

The defining feature of the month was not merely transaction volume, but the sophistication of the capital structures being deployed. Canadian issuers, advisors, governments, strategic investors, and institutional lenders are increasingly collaborating through layered financing architectures that blend public equity, structured debt, streaming agreements, strategic industrial partnerships, and quasi-sovereign capital. This evolution reflects a broader transformation in how major industrial and resource projects are financed in the modern economy.

Looking ahead, the trends visible in April 2026 are likely to persist through the remainder of the year:

Continued strength in critical minerals and strategic resource financing

Expanded use of hybrid debt/equity structures

Increased participation from sovereign and quasi-sovereign capital

More infrastructure-style financing models for industrial projects

Selective software and portfolio-rationalization transactions

Ongoing emphasis on balance-sheet optimization and refinancing activity

In practical terms, April 2026 may ultimately be remembered as a month where the Canadian mid-market further evolved away from traditional middle-market M&A and toward a more strategic, globally connected, capital-intensive ecosystem centred on long-duration industrial transformation.

Risk Disclaimer and Intended Use: This report is intended to act as an educational resource, - not a definitive recommendation. Please reference underlying sources directly for further details. This report is not a recommendation to raise capital from investors, US-based or otherwise. If you need advice for your business, you are welcome to contact us for a referral.