Investment Banking in Canada: Key Players, Trends & Deal Activity (2021–2025)

The definitive guide to Canada’s investment banking landscape – discover the Big 5 banks and top boutiques, recent M&A deal volumes and hottest sectors, plus strategic insights for founders.

🔍 Executive Summary: Investment Banking Canada

Canada’s investment banking landscape is marked by a handful of dominant domestic banks, an active mid-market, and a recent boom-and-cool cycle in deal activity.

Readers will learn:

Who the major players are (from the Big Five banks to boutique advisors),

how record-breaking M&A in 2021 gave way to a slowdown in 2022–2023, which sectors drove the most deals, and

why Canada’s mid-market remains a resilient engine of transactions.

We’ll unpack the numbers – total deal volumes, counts, and sector leaders – and provide insights on how founders, investors, and policymakers can navigate this evolving scene.

In short, this report is a one-stop briefing on Canada’s investment banking arena.

🧩 Why Investment Banking in Canada Matters

Canada’s investment banking sector may be smaller than its U.S. counterpart, but it punches above its weight in facilitating economic growth and corporate evolution (mergersandinquisitions.com).

Why is this topic timely? After a frenzy of deal-making in late 2020 and record highs in 2021, the environment has shifted with rising interest rates, inflation, and global uncertainties dampening mega-deals (newswire.ca).

Yet, mid-market M&A has proven resilient, buoyed by a wave of retiring business owners looking to sell (an estimated $2 trillion in Canadian business assets could change hands in the next decade as baby boomers retire - newswire.ca). This means a steady pipeline of mergers, acquisitions, and financing needs – a critical juncture for Canada’s economy.

Equally important, Canada’s economic priorities (from tech and renewable energy to critical minerals and infrastructure) are driving strategic transactions.

The federal push for clean energy and digital innovation has spurred deals in those sectors, while the global energy transition and U.S. trade dynamics influence cross-border activity.

Investment banking is the engine connecting capital to opportunity, whether it’s helping a Toronto tech startup raise growth capital or advising on a Calgary oil patch merger.

Understanding the key players and trends in Canadian IB isn’t just academic – it’s vital for founders eyeing exits, investors hunting deals, and policymakers aiming to foster a competitive market.

In short, the Canadian deal landscape is at an inflection point, balancing post-pandemic adjustments with new growth avenues. Now is the time to grasp what’s happening under the hood.

💡Investment Banks in Canada: Key Insights

💰 Deal Boom and Cooldown:

Canadian M&A activity surged to all-time highs in 2021 (over 4,500 deals worth $507 billion USD, a 10-year record) before falling ~44% in value in 2022 amid market volatility (imaa-institute.org). Deal count dropped ~22% year-over-year, reflecting a broad cooldown from the 2021 frenzy.

2023 saw further softening in deal volume (estimated ~2,990 deals, $269 billion) but with only a modest 5% value dip as a few megadeals propped up totals (imaa-institute.org).

In short, 2021 was a blockbuster, 2022–2023 a correction, and late 2024 shows early signs of a rebound.

🏦 Big Banks Dominate the Scene:

The Big Five banks – Royal Bank of Canada (RBC), Toronto-Dominion (TD), Bank of Montreal (BMO), Scotiabank, and CIBC (plus National Bank as a “Big 6”) – form the backbone of Canada’s investment banking landscape, especially for domestic equity and debt underwriting (mergersandinquisitions.com).

They consistently top league tables in Canadian equity/debt issuance and mid-sized M&A. For example, RBC Capital Markets is routinely ranked the #1 investment bank in Canada and was the only Canadian firm among the global top 25 M&A advisors in 2022 (investmentexecutive.cominvestmentexecutive.com).

These banks leverage deep local networks and balance sheets to dominate home-market deals, while partnering with global banks on cross-border megadeals.

🌍 Cross-Border Influence & Global Players:

Bulge-bracket global banks (Goldman Sachs, JP Morgan, Morgan Stanley, etc.) and elite boutiques (Evercore, Lazard, Rothschild) are active in Canada primarily on large, cross-border transactions (mergersandinquisitions.com, mergersandinquisitions.com).

Many of Canada’s biggest deals involve foreign buyers or targets, so U.S. and international advisors often join forces with Canadian banks. (Case in point: the $31 billion CP–KCS railroad merger, spanning Canada, the U.S. and Mexico, had both Canadian and U.S. banks advising.)

Cross-border M&A typically accounts for roughly half of Canadian deal value in a given year, underscoring Canada’s integration into global capital markets. RBC’s international clout is growing – its $13.5 billion purchase of HSBC Canada (2022) was billed as a move to boost global presence (reuters.com, reuters.com) – but U.S. giants still lead on the very largest global deals.

🤝 Mid-Market Resilience:

Beneath the headline megadeals, mid-market transactions (EV ~$10M–$500M) are the lifeblood of Canadian M&A.

Deals under $500M consistently make up about 75% of all transactions by count (torys.com).

In 2022, there were 2,618 mid-market deals (Refinitiv data) – a huge volume that barely makes the front page but adds up to significant economic impact (newswire.ca).

Even as IPOs and billion-dollar mergers cooled in 2022, mid-market M&A held steady, supported by record private equity dry powder and an oncoming wave of founder succession sales (newswire.canewswire.ca).

Notably, advisory firms like KPMG Corporate Finance have thrived here – KPMG advised on 55 mid-market deals in 2022, more than any other firm (newswire.ca).

The takeaway: Canada’s mid-market is highly active and relatively insulated from the extremes of the market cycle, providing a stable base of deal flow.

📈 Hottest Sectors:

The sector mix of deals has evolved, with a few standouts in recent years. Financial services and real estate led 2022’s deal roster – REITs topped the chart with $32.7 B in M&A, and banking/financial companies saw a combined $44 B in deals including the RBC/HSBC merger (bennettjones.com, bennettjones.com).

Technology has been vibrant:

Software companies saw ~$19 B in deals in 2022bennettjones.com, and tech M&A has continued as valuations reset (for example, Canada’s Magnet Forensics and Benevity were snapped up by PE in 2023).

Energy is in flux:

Renewables and clean energy actually outpaced oil & gas in deal value in 2022 – together totalling ~$29.3 B (bennettjones.com) – as investors pivot to green assets.

That said, traditional oil & gas still saw strategic consolidation (e.g. gas utilities and upstream asset sales) once commodity prices stabilized.

Mining deserves a shout-out: over $11 B in mining deals in 2022 and the highest deal count of any sector (bennettjones.com), reflecting Canada’s rich critical minerals focus (expect more action here due to EV battery metals demand).

In short, financials, real estate, tech, and energy/mining are Canada’s M&A hotbeds, with each contributing major transactions.

⚖️ Canadian Regulatory & Economic Backdrop:

Canada’s dealmaking is shaped by a unique regulatory environment and recent economic swings. On the regulatory side, large acquisitions may trigger reviews – e.g. telecom mergers face Competition Bureau scrutiny (as Rogers–Shaw learned), and foreign takeovers in “sensitive” sectors like critical minerals or banking require federal approval (the government in 2022 even ordered divestitures of some Chinese investments in mining - nortonrosefulbright.com).

This can add complexity and influence deal structure (sometimes requiring remedies like asset sales to get approved).

Economically, rising interest rates and recession fears in 2022–2023 dampened valuations and made financing costlier, contributing to the slowdown in big deals (newswire.ca).

However, Canada’s strong banking system and trillions in institutional capital (pension funds, PE funds) kept liquidity flowing. The result: fewer but larger deals – 2023’s average deal size jumped with 55 megadeals closing (vs 60 in 2022) and total value actually +47% higher than 2022 despite lower deal count (kroll.comkroll.com).

Investors adapted with creative deal structures (earn-outs, spin-offs) and a focus on strategic fits to get deals done in a tougher climate.

The insight here is that policy and macroeconomics directly influence deal trends – a factor any dealmaker in Canada must heed.

🛠 How It Works – The Canadian Deal-Making Process, Step by Step

Investment banking in Canada facilitates a range of transactions – from M&A deals to equity financings – through a fairly standard process. What follows is a simplified step-by-step breakdown of how a typical deal works, with some Canadian twists along the way:

Mandate & Advisor Selection:

It all starts when a company or its shareholders decide on a strategic move – say, selling the business, acquiring a competitor, or raising capital. They’ll mandate an investment bank or advisory firm to represent them.

In Canada, this could be a big bank’s advisory arm (e.g. RBC Capital Markets for a large public company) or a specialized boutique for mid-market deals (e.g. Canaccord Genuity, Deloitte Corporate Finance, etc.).

The choice often hinges on the deal size and industry focus – mining firms might hire BMO for its metals & mining expertise (mergersandinquisitions.com), while a tech startup might go with a boutique specialist. The advisor and client define the objectives, valuation expectations, and process timeline.

Preparation & Valuation:

The investment bankers perform valuation analysis (using DCF, comparables, etc.) to establish a price range and strategize deal terms.

They also get busy preparing marketing documents – for M&A, a confidential information memorandum (CIM) that profiles the company is drafted; for a financing, a prospectus or investor presentation is readied.

In Canada’s tight-knit markets, advisors pay close attention to confidentiality and regulatory rules (like not tipping off markets before material announcements. At this stage, the bank identifies and quietly approaches potential counterparties. For example, if selling a mid-sized manufacturing firm, the advisor will draw up a list of likely buyers (including U.S. or international players, given cross-border interest is high). Local knowledge is key – Canadian advisors leverage networks across Toronto, Montreal, Calgary, etc., often tapping U.S./global investors since half of deals involve cross-border parties.

Marketing & Bids:

Once initial prep is done, the deal moves into outreach. The advisor (with client approval) contacts prospective buyers or investors, shares the CIM under NDA, and begins management meetings.

In a financing scenario (like an IPO or private placement), this is when the bankers and management go on an investor roadshow. Canadian deals often have a smaller pool of domestic institutional investors, so for larger deals bankers will court U.S. and global investors to ensure strong demand.

Over a few weeks, indications of interest or non-binding bids come in. For an M&A sale, the bankers might run an auction process – soliciting bids, then shortlisting a few parties for deeper due diligence.

In Canada’s mid-market M&A, it’s common to have multiple family-owned buyers or U.S. private equity firms in the mix, given the sheer number of retiring owners selling businesses (newswire.ca). The advisor’s role here is part matchmaker, part coach – ensuring bidders see the strategic fit and competitive urgency.

Deal Negotiation & Structuring:

As final bidders emerge or an investor is ready to commit, the investment bankers help negotiate key terms. This includes price (valuation), but also the structure: Will it be an all-cash acquisition or stock swap? Any earn-outs or contingent payments? For financings, what will the pricing of the new equity or debt be?

Canadian deal structuring must account for tax efficiency (e.g. using a flow-through share structure for mining financings) and regulatory nuances (for instance, ensuring a foreign buyer’s offer structure can clear Investment Canada Act review if needed). The advisors work closely with lawyers at this stage to paper the term sheet or definitive agreement.

In 2022–2023, material adverse change (MAC) clauses and interim morality covenants got extra scrutiny in Canadian M&A, thanks to pandemic-era legal cases (like Cineplex vs. Cineworld) highlighting the importance of specific terms (torys.comtorys.com). A good Canadian IB advisor is adept at navigating these details to protect their client’s interests while keeping the deal attractive to the other side.

Due Diligence & Approvals:

Before a deal is finalized, extensive due diligence takes place. Buyers scour the target’s financials, operations, and risks – investment bankers coordinate this diligence process, setting up data rooms and Q&A sessions.

In a capital raise, investors perform due diligence on the company’s metrics and market position. Concurrently, any required regulatory approvals are sought.

In Canada, this can include: Competition Bureau approval for mergers that lessen competition; OSFI approval for bank mergers (e.g. RBC’s takeover of HSBC Canada required sign-off from the Finance Minister - reuters.com); and Investment Canada Act review for major foreign investments (especially in areas like telecom, finance, or critical minerals – where the government can block deals not seen as a “net benefit to Canada”). A recent example is Rogers’ $26 B acquisition of Shaw, which required a lengthy review and divestiture of Shaw’s wireless assets to Quebecor to get approval (telecomreviewamericas.com). Investment bankers often help navigate these hurdles, structuring remedies or lobbying as needed because a deal only matters if it can close.

Closing & Integration:

With due diligence done and approvals in hand, the deal moves to signing and closing. Investment bankers coordinate the closing logistics – finalizing financing (e.g. finding a lender to fund part of an acquisition, or allocating shares in an IPO to investors).

On closing day, funds and assets are exchanged per the agreement. Deal toys are arranged or tombstones are printed (yes, the ceremonial Lucite plaques are still a tradition!) and the news is announced publicly.

But the work isn’t over: bankers often assist clients with post-merger integration strategy or market positioning after a transaction. For instance, after a merger, keeping the investor community informed on synergy realization can support the stock price – an area where equity capital markets bankers advise.

In the case of mid-market entrepreneurs selling their company, bankers might also counsel on wealth management or reinvestment options post-sale (passing the baton to other divisions of the bank). When all is said and done, the IB team ensures the client is set up to realize the intended value of the deal. And of course, they hope to leverage a successful transaction into a long-term advisory relationship for future deals.

Overall, the investment banking process in Canada mirrors global M&A processes with a few distinct flavours – smaller market dynamics, closer regulatory oversight in certain sectors, and a heavy cross-border component.

The end-to-end involvement of Canadian advisors, from strategy through closing, makes them trusted partners to businesses navigating transformative transactions.

📊 Data, Trends & Case Studies Across Canada’s Investment Banking Landscape

Let’s dive into the numbers and real-world examples that illustrate Canada’s investment banking activity in recent years. The data paints a clear picture of a roller-coaster ride: a 2021 deal surge, a 2022 pullback, and a 2023 stabilization with big deals still happening. Meanwhile, case studies show how these trends played out on the ground.

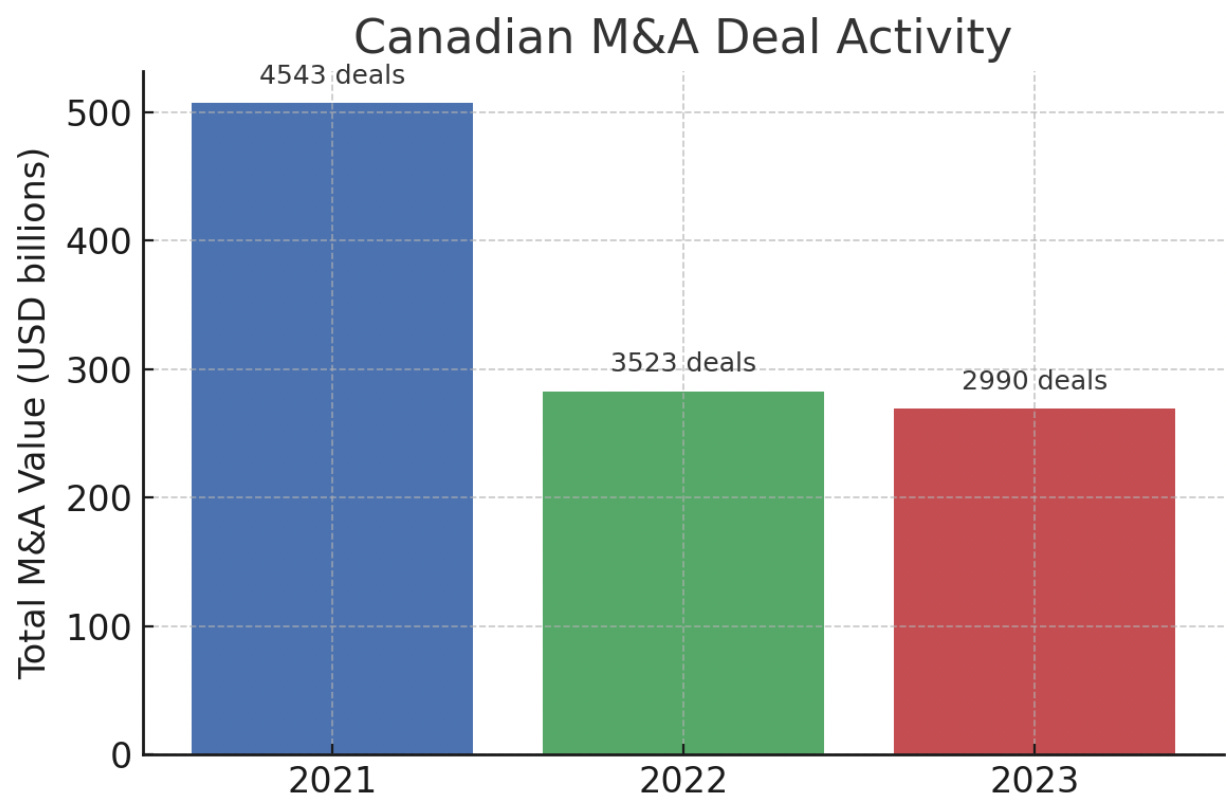

Figure: Canadian M&A deal activity by year (2021–2023), showing total announced deal value (USD) and number of dealsimaa-institute.orgimaa-institute.org. 2021 shattered records with ~$507 B in deals (4,543 transactions) – then 2022saw a sharp drop to ~$282 B (3,523 deals) as markets cooled. 2023 (projected ~$269 B, ~2,990 deals) leveled off in value with fewer but larger deals, highlighting the impact of megadeals in boosting total value.

Deal Volume & Value Trends: The chart above underscores the dramatic swing. 2021’s boom was fuelled by ultra-low interest rates, pent-up demand after 2020’s lull, and several blockbuster deals (more on those shortly).

In fact, 2021’s $507 B in Canadian deals was not only a 10-year high (torys.comtorys.com) but truly unprecedented – it included multiple $10B+ transactions that collectively turbocharged the stats.

The 2022 decline (–44% in value via imaa-institute.org) mirrored global trends, as inflation and rate hikes hit and valuations normalized. Many would-be acquirers hit pause amid market uncertainty, and the IPO window essentially shut (2022 saw far fewer new issues than 2021’s IPO rush).

Interestingly, deal count fell only ~22% (imaa-institute.org) – meaning lots of smaller deals still happened, but the absence of supersized mergers cut the dollar value dramatically.

By 2023, Canada’s M&A market found a new equilibrium: overall deal count continued to slip (on pace for ~15% fewer deals than 2022 - imaa-institute.org), but total value was only ~5% lower as several megadeals landed in 2023 (imaa-institute.org).

For example, Rogers Communications’ long-awaited $26 B takeover of Shaw closed in 2023, adding a big chunk. Additionally, the first half of 2025 has seen a resurgence – in just H1 2025, deal value spiked ~65% year-on-year thanks to huge announcements (like Enbridge’s $19 B utility acquisition - ionanalytics.com – suggesting the lull may be over. The cyclical nature of M&A is on full display: feast, famine, and early signs of another feast ahead.

Canadian Mid-Market Stability:

While the headline numbers whipsawed, Canada’s mid-market deals (sub-$500M) quietly kept a steady cadence. As noted, about three-quarters of all deals are mid-market (torys.com).

In 2021, mid-market activity also hit high gear (reflected in an 18% jump in mid-sized public deals - torys.com). Come 2022, even as big deals waned, 2,618 mid-market deals closed, only a slight dip (newswire.ca). These included countless private company sales, tuck-in acquisitions by larger companies, and private equity roll-ups.

Private equity in particular remained very active – 2022 saw record PE fundraising and those funds kept shopping for mid-sized Canadian firms (the KPMG data shows PE-backed deals held strong - newswire.ca). For instance, many family-owned manufacturers in Ontario or Alberta changed hands to financial sponsors or to industry consolidators.

The mid-market has been resilient for a structural reason: demographics.

There’s a large cohort of aging SME owners in Canada (nearly half of primary business owners are 50–64 years old - newswire.ca), leading to a steady flow of succession-driven sales. This “silver tsunami” of business sales is a unique trend sustaining Canadian deal flow regardless of macro conditions.

Sector Spotlight – 2021 vs 2022: The sector composition of deals has shifted a bit from 2021’s peak to 2022’s cooldown:

Telecom & Media (2021): One of the biggest deals of 2021 was Rogers Communications’ $26 billion bid for Shaw Communications (torys.com), a game-changing telecom merger. Along with that, a major media deal saw Couche-Tard (a convenience store giant) attempt a large foreign acquisition (though it ultimately didn’t proceed). These helped make TMT (Tech, Media, Telecom) a large share of 2021 values.

Transportation (2021): Another colossal 2021 deal: Canadian Pacific Railway’s $31 billion acquisition of Kansas City Southern (KCS) (reuters.com), to create a transcontinental railway. This cross-border deal showcased Canada’s ability to produce a North American mega-merger (approved in 2023) and boosted the industrials/transport sector’s deal value significantly.

Financial & Real Estate (2022):

In 2022, the financial sector exploded to the forefront – notably with RBC’s announced C$13.5 B purchase of HSBC Canada, the largest Canadian bank deal in decades (reuters.com).

Banks and diversified financial firms together accounted for $44.2 B in deals in 2022, one of the busiest years for financial services M&A on record (bennettjones.com, bennettjones.com).

Real estate also dominated: REITs led all sectors with $32.7 B in transactions (bennettjones.com). This included several large REIT privatizations and portfolio sales – for example, Blackstone and partners acquired Summit Industrial REIT for ~$5.9 B, and other institutional investors snapped up real estate assets to take advantage of high valuations and the low-rate environment early in the year.

Technology (2022): Tech stayed robust – software companies saw about $19 B in M&A value across 280 deals (bennettjones.com), ranking as the 5th largest sector by value. 2022 started hot for tech (following 2021’s tech frenzy), though it cooled by Q3 as interest rates climbed (nortonrosefulbright.com). A notable deal: OpenText (Waterloo-based) acquired Micro Focus for ~$6 B, highlighting Canadian tech firms’ appetite to grow via acquisitions even as valuations shifted.

Energy & Mining:

The energy picture flipped somewhat. Traditional oil & gas M&A was cautious in 2022, with high oil prices ironically stalling deals as sellers wanted peak valuations, buyers were wary (bennettjones.com).

Still, some deals happened as companies refocused portfolios (Cenovus, Suncor and others made targeted acquisitions/divestitures).

Meanwhile renewable energy assets were in high demand – Canadian investors engaged in lots of international clean energy deals (solar, wind, hydro) in 2022 (bennettjones.com).

Combined, renewables plus O&G tallied $29.3 B (bennettjones.com), but tellingly “there was more volume in alternate energy than in oil & gas” (bennettjones.com), reflecting the energy transition. Mining remained consistently active, particularly in the second half of 2022 as metal prices stabilized. A headline transaction was the merger of Agnico Eagle Mines and Kirkland Lake Gold (C$13.5 B) announced late 2021 and closed in 2022, creating a Canadian gold mining powerhouse. In 2023, mining M&A buzzed with talk of critical minerals consolidation (e.g. Glencore’s $23 B proposal for Teck Resources, and numerous lithium mining deals).

Case Studies – Notable Deals: Sometimes individual deals illustrate broader trends. Here are a few case snapshots from recent years:

Rogers–Shaw Merger (Telecom, $26 B):

Case: Announced in 2021 and closed in 2023 after lengthy regulatory battles, this deal saw Toronto-based Rogers acquire Western Canada-focused Shaw to form a telecom giant (telecomreviewamericas.com).

It highlights how Canadian mega-deals can face significant regulatory hurdles – the Competition Bureau initially opposed it, and final approval required Shaw’s mobile division (Freedom Mobile) to be sold to Quebecor to preserve competition. From an IB perspective, multiple banks were involved: RBC and TD advised Rogers, while CIBC advised Shaw.

The merger underscores the scale of domestic consolidation possible in Canada (it created Canada’s #2 telecom company) and the pivotal role of investment banks in navigating approvals and public scrutiny for such transformative deals.

RBC–HSBC Canada Acquisition (Banking, C$13.5 B):

Case: Announced late 2022, Royal Bank’s acquisition of HSBC’s Canadian subsidiary was a landmark banking deal – the largest bank takeover in Canada in 30 years (reuters.com).

HSBC decided to exit Canada, and RBC leapt at the chance to bolster its market share by ~130+ branches and $100B in assets. The deal demonstrates the dominance of Canada’s Big Banks: a Big 5 player absorbed the 7th-largest bank to get even bigger domestically (reuters.com).

It also required political approval; ultimately the Finance Minister cleared it in 2023, despite some concerns about reduced competition. (Notably, the government hadn’t allowed big bank mergers since the ’90s, so this was a unique situation.) Investment banks were key on both sides – RBC’s in-house team obviously drove their deal, and HSBC engaged advisors (JP Morgan, Goldman) to shop the unit.

The transaction underlines how foreign banks have struggled to compete with domestic giants and how IB-facilitated consolidation is shaping Canada’s financial sector.

CP–KCS Railway Combination (Infrastructure, $31 B):

Case: In late 2021, Canadian Pacific Railway outmaneuvered a rival bid to strike a deal with Kansas City Southern, a U.S. railroad, aiming to create the first ever Canada-U.S.-Mexico rail network.

It’s a prime example of cross-border M&A requiring multi-national approval – U.S. regulators (STB) only gave the green light in 2023 with conditions (reuters.com, reuters.com).

The complexity was enormous: two countries’ regulators, competing bidder (CN Rail) in the mix initially, and billions in financing. Advisors included BMO and Scotiabank on CP’s side and Morgan Stanley for KCS. This case study showcases Canadian firms’ ambition on the world stage and how investment banks help navigate everything from bidding wars to regulatory concessions (the deal included a voting trust structure to hold KCS during the long approval process).

The successful closing cemented CP – now CPKC – as a continental player and demonstrated that Canadian companies (with the right IB guidance) can execute mega-deals against global competition.

Mid-Market Family Business Sale (Industrial, ~$100 M):

Case: Consider a more typical mid-sized deal – in 2022, the owners of a Toronto-area auto parts manufacturer decided to sell their ~$100 million-revenue business as the founders approached retirement.

They hired a mid-market investment bank (in this case, KPMG Corporate Finance) to run a confidential auction. After reaching out to both Canadian and international strategic buyers and private equity firms, multiple offers came in.

The winning bidder was a U.S.-based automotive parts company looking to expand into Canada, who paid ~8x EBITDA (~$120 M) for the company. This relatively small transaction (by Bay Street standards) didn’t make headlines, but it’s emblematic of thousands of such deals happening across Canada. The role of the investment banker was crucial – finding an overseas buyer willing to pay a premium and structuring the deal (including earn-outs for the founders and employment contracts for key managers to stay post-sale).

This example typifies how mid-market IB connects entrepreneurs to global capital, often quietly creating wealth and smoothing generational transitions without fanfare.

Private Equity Takeover – Magnet Forensics (Tech, $1.8 B):

Case: In early 2023, Magnet Forensics, a Waterloo-based cybersecurity software firm (founded by a former police officer) agreed to be acquired by U.S. private equity firm Thoma Bravo for around C$1.8 billion. Magnet was a TSX-listed company, and the deal was structured as a plan of arrangement, taking Magnet private.

This illustrates a few trends: Canadian tech companies often become acquisition targets for large U.S. PE funds, which see value in Canada’s tech talent and products (especially when valuations dip).

Also, it shows how investment banks facilitate fair outcomes – Magnet’s board formed a special committee and hired advisors (BMO Capital Markets) to negotiate with PE and ensure shareholders got a good price. After some shareholder pushback that the initial offer was too low, Thoma Bravo sweetened the bid. The deal went through, giving Magnet the capital and partners to grow globally.

The takeaway: Canada’s vibrant tech scene feeds into M&A, and IB advisors play a key role in bridging the gap between entrepreneurial companies and the deep pockets of private equity.

These case studies – from headline-grabbing mergers to bread-and-butter business sales – collectively demonstrate the spectrum of Canadian investment banking activity.

They highlight the central role of investment banks as enablers and negotiators, whether it’s a transformative merger reshaping an industry or a discreet sale securing a founder’s retirement.

In each case, the outcomes (good or bad) hinged on understanding the market, buyers, and regulatory context – precisely the expertise that top Canadian advisors bring to the table.

🧭 Strategy Playbook – Actionable Insights for Founders, Investors & Policymakers

What can various stakeholders do with this knowledge about Canada’s investment banking and deal landscape? Here’s a strategy playbook with actionable guidance:

For Founders & Business Owners (Considering Exits or Capital Raises):

✅ Plan Early for Succession or Sale:

If you’re an owner eyeing retirement or liquidity, start prepping 2–3 years in advance. Get your financials in order, streamline operations, and address any skeletons in the closet (legal, compliance issues) that could scare off buyers.

Early planning can significantly boost your valuation – buyers pay for well-run, low-risk businesses.

Given that 75% of small biz owners may retire in the next decade (newswire.ca), a solid succession plan (whether family takeover or external sale) is essential to stand out in a crowded market of sellers.

💰 Engage the Right Advisors:

Don’t go it alone on a major deal. Tap into Canada’s robust network of investment banking advisors or M&A boutiques that specialize in your size range and industry.

A good advisor will run a competitive process to get you the best price and terms.

For a mid-market firm, that might be a boutique or Big-4 corporate finance team that has relationships with the most likely buyers (including U.S. players who often pay a premium for Canadian targets).

Their fees are well worth the value they can add through negotiation savvy and deal structuring.

📊 Know Your Value & the Market:

Work with your advisor to realistically value your business and identify your “story” for investors. Is your sector hot (tech, healthcare)? Are you demonstrating growth or resilience?

In 2021, sellers enjoyed peak valuations; in 2023, buyers became choosier. Understand current multiples in your sector and be ready to justify yours with data.

Also, gauge the buyer universe: e.g. if U.S. private equity has been acquiring similar firms in Canada (as in many tech and healthcare niches), use that as leverage – they might pay more given strategic intent.

🤝 Be Open to Creative Deals:

Not every sale is 100% cash upfront. Especially in uncertain times, earn-outs, minority recapitalizations, or partial equity rollovers are common. For instance, you might sell 70% now to a PE fund and retain 30% to sell later (betting on future growth).

Or accept an earn-out where you get more if the company hits targets post-sale. These structures can bridge valuation gaps between you and the buyer.

Be open-minded – with good legal and financial advice to safeguard your interests, creative deals can maximize your total payout.

⚠️ Preserve Business Momentum:

During a deal process, it’s easy to get distracted by negotiations and due diligence. But remember, your business must keep performing up to closing (and ideally beyond, if you’re sticking around).

Many deals have fallen apart because the target hit a sudden slump or lost key staff/customers mid-process.

Keep it confidential as much as possible (to avoid unsettling employees and clients), and lean on your advisors to handle the heavy lifting so you can focus on running the business.

A stable, growing business through closing not only ensures the deal closes, it might also trigger that earn-out or valuation bump you negotiated.

For Investors & Corporate Acquirers (Seeking Opportunities in Canada):

💡 Map the Landscape & Build Relationships:

If you’re a private equity investor or a corporate M&A team from abroad, do your homework on Canada’s industry clusters and key players.

Canada has unique pockets of excellence – e.g. Toronto/Waterloo for tech and fintech, Montreal for AI and gaming, Calgary for energy tech, Vancouver for biotech, etc.

Plug into local networks: many deals in Canada are relationship-driven. Cultivate connections with Canadian investment bankers and brokers who can tip you off to opportunities before they go broad. Regularly attending Canadian industry conferences or events can put you on the radar for deal flow.

💰 Leverage Canada’s Favourable Investment Climate:

Canada is quite open to foreign investment (with a few sector exceptions), and it offers advantages like a skilled workforce and strong rule of law.

For U.S. investors, the geographic and cultural proximity is a bonus. Take advantage of valuation gaps – historically, some Canadian companies trade at lower multiples than U.S. peers, so acquisitions can be value-accretive.

For instance, Canadian mid-cap tech or industrial firms might be cheaper buys for U.S. PE funds that arbitrage the difference. That said, be mindful of currency (CAD vs USD) and get tax structuring advice to optimize cross-border deals.

🧐 Focus on Hot Sectors & Consolidation Plays:

As outlined, financial services, tech, clean energy, and mining are ripe areas. If you’re a corporate looking for a tuck-in, Canada’s fintech and software startups offer cutting-edge innovation at reasonable sizes. (E.g. many U.S. fintechs have acquired Canadian startups to expand into the market.)

If you’re a PE fund, note that fragmented industries like healthcare services, IT consulting, or manufacturing present roll-up opportunities – you can assemble regional players into a national platform.

Also watch the energy transition: with government incentives in renewables and carbon tech, acquiring Canadian clean energy projects or firms can be strategic. The key is to identify where Canada’s strengths align with your growth thesis.

🤝 Engage Local Partners:

Consider partnering with Canadian co-investors or JV partners, especially in regulated sectors.

Canada’s large pension funds (e.g. CPPIB, Ontario Teachers’) and families often co-invest and can smooth the path with their local knowledge.

For example, big infrastructure deals often see a foreign investor team up with a Canadian pension fund to win the asset – combining global capital with local credibility. In the middle market, Canadian search funds and family offices might co-sponsor deals.

A partnership approach can also appease government concerns for foreign buyers (showing the asset will have some Canadian ownership/oversight).

⚠️ Prepare for Due Diligence & Approvals:

If you’re acquiring in Canada, don’t underestimate the regulatory layer. Even if a formal Investment Canada Act review isn’t triggered, politicians pay attention to major foreign takeovers.

Have a plan to demonstrate how your investment is a “net benefit” to Canada – job creation, keeping decision-making in-country, etc., can help your case. Also, engage Canadian legal counsel early to navigate competition law (the Competition Bureau has gotten more assertive lately).

On diligence, watch for Canadian-specific issues like First Nations consultation rights on resource projects, bilingual (French) requirements in Quebec operations, or provincial regulations that might differ from U.S. norms.

Thorough due diligence and a proactive government relations strategy will increase your odds of a smooth closing.

For Policymakers & Ecosystem Builders (Fostering a Healthy IB Environment):

🏦 Support Competitive Capital Markets:

A vibrant investment banking sector requires robust capital markets. Policymakers should ensure Canadian public markets stay attractive for companies to list and raise capital.

This could include reviewing regulatory burdens for IPOs and potentially easing some compliance costs for smaller issuers, so more startups choose TSX/TSXV listings over a U.S. sale.

Recent years saw many tech firms opt for U.S. SPACs or acquisitions instead of Canadian IPOs – reversing that trend could keep more growth at home.

Supporting initiatives like the Toronto Stock Exchange’s Sandbox (which encourages innovation in listings) or the growth of venture exchanges will strengthen the domestic IB pipeline.

💰 Encourage Investment & Succession Solutions:

With the wave of SME owners retiring, government programs can help facilitate smoother transitions and keep businesses alive (instead of just shutting down for lack of a successor).

Expand programs like the Business Development Bank of Canada (BDC) growth & transition capital, which provides mezzanine financing for management buyouts or family transitions.

Tax incentives for inter-generational business transfers (recently introduced to level the tax treatment of family business sales vs external sales) are a positive step – continue refining those to remove unintended barriers.

The government might also consider co-investment funds or guarantees to encourage private equity and banks to finance more mid-market deals, ensuring viable businesses can be sold to the next generation of entrepreneurs or investors.

🌎 Maintain Openness but Protect Key Interests:

Striking the balance on foreign investment is crucial. Canada has largely benefited from being open to global capital – it brings know-how and market access.

Policymakers should continue to promote Canada as an investment destination (the stability and resource wealth are big draws) while judiciously using tools like the Investment Canada Act for genuinely sensitive cases (e.g. military tech or critical minerals going to state-owned enterprises of concern).

The new guidelines in 2022 tightening SOE investment in critical minerals (iea.org, nortonrosefulbright.com) are understandable for national security; however, for most sectors, a clear and fair review process is needed so that foreign M&A isn’t scared away by uncertainty. In short: keep the welcome mat out for investors, with transparent rules of the road.

🤝 Facilitate Innovation & Networking:

Government and industry bodies can help build the ecosystem that underpins investment banking deal flow. This includes funding innovation clusters (so that more startups grow locally to a scale that warrants IPOs or big-ticket M&A) and supporting incubators/accelerators. More successful domestic companies mean more work for Canadian IBs and more economic benefits at home.

Additionally, Canada could bolster its position as a hub for international dealmaking – e.g. hosting global conferences in Toronto or Montreal on mining finance or fintech investment. Such events can draw international investors and promote deal flow with Canadian firms (and concurrently raise the profile of our investment banks).

Essentially, policymakers can act as cheerleaders and conveners to make sure the world knows Canada is open for business and brimming with opportunities.

📈 Data & Transparency: Finally, a nerdy but important point – improving the tracking and transparency of M&A and financing data in Canada.

Often, data on private deals is piecemeal. If the government (or perhaps a partnership with data providers) could aggregate and publish more comprehensive stats on mid-market M&A, it would help policymakers and investors alike to identify trends early.

Knowing which sectors have lots of small deals (signaling maybe need for scale-up support) or where foreign buyers are concentrating (signaling strengths or vulnerabilities) can inform smarter policies. In essence, measure it to manage it.

Canada has organizations like ISED and StatsCan that could work with the IB community to enhance market data – a boon for decision-making in both public and private sectors.

By following these playbook strategies, founders can maximize their outcome, investors can seize opportunities smartly, and policymakers can cultivate a thriving environment.

When each stakeholder plays their part, Canada’s investment banking ecosystem becomes more dynamic, inclusive, and beneficial to the broader economy.

The goal is a virtuous cycle: strong companies attract capital, successful deals create wealth and confidence, and that, in turn, fuels the next generation of entrepreneurs and investors.

🇨🇦 Canadian Angle – What Makes Canada Unique in the IB World

Even though investment banking fundamentals are global, Canada’s context adds a unique flavor to how deals are done. Here are a few distinct angles to bear in mind, highlighting Canadian programs, players, and cultural factors:

Homegrown Financial Stability:

Canada’s banking system is renowned for its stability – the World Economic Forum has often ranked it among the soundest globally. This stability (no major bank failures in decades) means Canadian investment banks operate from a position of strength and trust.

During global downturns, Canada often fares relatively well, which attracts foreign capital to Canadian deals as a “safe haven.” For example, during the 2022–2023 volatility, global investors remained keen on Canadian infrastructure and real estate assets, viewing them as lower risk.

The Big Six banks, being universal banks, also have strong balance sheets to lend and underwrite through cycles, which kept deal pipelines alive (underwriting loans for acquisitions when U.S. credit markets got jittery in 2022).

Public-Private Dealmakers – The Power of Pension Funds:

A uniquely Canadian phenomenon is the outsized role of Canadian pension funds in M&A and investments. Giants like CPP Investments, Ontario Teachers’ Pension Plan, CDPQ, PSP, and others are not just passive investors; they often act like global private equity firms.

They directly acquire companies, infrastructure, real estate, and even participate in tech buyouts. For instance, CPPIB co-led the ~$15 B take-private of software firm Qualtrics in 2023 (kroll.com, kroll.com) alongside Silver Lake – showing a Canadian fund driving a major international deal.

These pension funds frequently partner with investment banks on transactions (sometimes as clients, sometimes as co-investors), and they bring patient capital with a Canadian flag.

For Canada’s IB landscape, this means some of the biggest “buyers” in deals are domestic public institutions – a source of pride and a competitive advantage, as they often favor using Canadian advisors and have deep knowledge in sectors like infrastructure and resources.

Government Programs & Funders:

The Canadian government and provincial governments have several programs that indirectly support investment banking activity by spurring innovation and company growth.

For example, the Venture Capital Action Plan and funds-of-funds programs have bolstered VC in Canada, leading to more startups maturing. Agencies like BDC Capital and Export Development Canada (EDC) provide financing and guarantees that help companies expand (often leading to M&A or attracting IB attention for IPOs).

The Strategic Innovation Fund invests in large projects (like EV battery plants, cleantech, etc.), which can catalyze industry clusters and subsequent deals. On the flip side, regulatory policies like the recent Critical Minerals Strategy mean that certain mining deals now get extra scrutiny or support – e.g. the government created a Critical Minerals Development Program that could co-invest with private firms.

All these initiatives shape where investment bankers focus – if government is pouring money into say, hydrogen energy, bankers will be there lining up private investors for complementary deals.

In sum, the public sector in Canada often works hand-in-hand with private capital, and smart dealmakers keep a close eye on these programs to leverage them in transactions.

Cultural & Regional Nuances:

Canada is a vast country with regional economic hubs:

Toronto (Bay Street) dominates finance,

Montreal has its financial scene (with French-language business culture and unique Quebec laws to consider in deals),

Calgary is the energy capital (where O&G deals rise and fall with oil prices), and

Vancouver connects to Asia-Pacific capital flows. Investment banking in Canada often requires navigating these regional nuances.

For instance, a deal involving a Quebec company might see the advisor bringing in a Quebec-based partner or ensuring French-language transaction documents – a consideration less common elsewhere. Western Canada’s deals might involve different player networks (e.g. Calgary’s many boutique energy advisory firms). Canada’s strong cultural focus on ESG (environmental, social, governance) is also notable – Canadian investors and regulators put a premium on environmental and social impact of deals. A mining acquisition today might be scrutinized for Indigenous partnership opportunities or ESG commitments, and investment bankers increasingly highlight those aspects in pitches. All told, while Canada shares similarities with U.S./UK dealmaking, a successful Canadian IB professional is attuned to the country’s bilingual business environment, regional economies, and collaborative ethos.

Mid-Market Ecosystem & Government Support: Lastly, the mid-market, given its importance, has a well-developed ecosystem in Canada that is often supported by government or quasi-government bodies. For example, provincial securities commissions have tailored rules for “small business issuers” to raise capital more easily. The TSX Venture Exchange is a unique platform that allows very small companies to go public and grow – something few countries have. The result is many mining and junior tech companies list early, raising public funds when in other countries they might remain private – this creates work for investment banks in equity raises and M&A even at small scales. Governments often sponsor trade missions and matchmaking events for mid-sized companies (to help them find foreign investors or M&A partners). And organizations like the Canadian Innovation Exchange (CIX) or regional innovation hubs frequently invite investment bankers to meet emerging companies. The bottom line of the Canadian angle is a highly connected ecosystem where banks, funds, governments, and businesses interact closely to drive growth. It’s a smaller pond than the U.S., which means reputations matter a lot – trust and long-term relationships are the currency on Bay Street as much as pure dollars.

In summary, Canada’s investment banking environment is characterized by stability, strong domestic institutions (banks and pensions), supportive public policy in many areas, and a collaborative, relationship-driven culture.

These factors set Canada apart and often make it an attractive place to do deals – as well as a marketplace with its own idiosyncrasies. International players who understand the “Canadian way” can thrive here, and domestic players leverage these strengths to punch above their weight globally.

Canada might not have the sheer volume of Wall Street or the glitz of Silicon Valley, but it consistently delivers high-quality deal flow, world-class expertise, and a reliable investment climate – truly a case of “small but mighty” on the world stage of finance.

🏁 Bottom Line: Investment Banking in Canada

Canada’s IB Heavyweights & Allies: The Big 5 (RBC, TD, BMO, Scotiabank, CIBC) – plus National Bank – dominate domestic investment banking, especially in capital markets, while global banks and boutiques chime in on big cross-border deals. A robust mid-tier of accounting firms (KPMG, Deloitte, etc.) and boutiques handle the huge volume of mid-market deals, making Canada’s advisory landscape competitive and comprehensive (mergersandinquisitions.com, newswire.ca).

Deal Flow Whiplash: After a record-smashing 2021 for M&A (over $500 B in deals (imaa-institute.org), thanks to megadeals like Rogers–Shaw and CP–KCS), 2022 saw deal value plunge ~44% amid market turmoil (imaa-institute.org). Activity stabilized in 2023 with fewer deals but bigger sizes – showing Canada’s deal pipeline is down but not out, and poised for an uptick as conditions improve (imaa-institute.org). Mid-market transactions (≤$500M) remained a rock, comprising ~75% of all deals and keeping bankers busy even in slower times (torys.com).

Sectors in the Spotlight: Financial services and real estate led recent deal value, highlighted by big bank mergers and REIT takeovers in 2022 (bennettjones.com). Tech and software continue to drive many deals (nearly $19 B in 2022 (bennettjones.com), plus a stream of 2023 PE tech buyouts), while energy M&A is bifurcated – oil & gas deals rebounded cautiously as prices levelled, but clean energy and mining have surged with double-digit billion-dollar volumes (bennettjones.com). Expect critical minerals, renewables, and tech to stay hot as strategic priorities fuel those sectors.

Opportunities & Playbook: Founders should capitalize on Canada’s seller-friendly environment for solid mid-sized businesses – many buyers (including foreign) are eager, so prepare well and get expert advisors to maximize value. Investors (PE and corporates) eyeing Canada can find high-quality companies at reasonable multiples, especially in fragmented sectors – but must navigate local nuances (bilingual Quebec, foreign investment reviews) and consider teaming with Canadian partners for smoother deals. Policymakers can further boost the ecosystem by keeping markets open and fair, supporting SME transitions, and championing innovation clusters that produce the next wave of IPOs and M&As.

Canada’s Edge: Stable, trusted banks; enormous pension funds; an educated workforce; and a collaborative business culture give Canada an edge in attracting capital and executing deals. The country’s IB sector is “Harvard meets hockey” – sophisticated and globally savvy, yet down-to-earth and team-oriented. The bottom line for any reader: Investment banking in Canada is alive and kicking, bridging billions in capital with opportunities, and if you’re a player in this space (founder, investor, or official), knowing the key actors and trends outlined here will empower you to make the most of Canada’s dynamic deal landscape.

🧾 Final Word: Canada’s Deal Engine Is Still Running Strong

Despite global uncertainty and shifting economic tides, Canada’s investment banking sector remains resilient, adaptive, and full of opportunity.

From the record-breaking highs of 2021 to the recalibrated deal landscape of 2023–2024, the country has proven its ability to navigate complexity while fuelling both mega-mergers and mid-market transitions.

The Big 5 banks anchor the system, but it’s Canada’s blend of local expertise, global reach, and a strong middle-market fabric that keeps capital flowing. Whether you’re a founder planning a legacy-defining sale, an investor scouting high-quality assets, or a policymaker shaping the rules of engagement, understanding this dynamic ecosystem isn’t optional, it’s essential. Canada isn’t just open for business, it’s quietly closing deals that shape the future.

If you liked this research, check out our other free research reports on the Canadian Financing ecosystem.

Risk Disclaimer and Intended Use: This guide is intended to act as an educational resource, - not a definitive recommendation. Please reference underlying sources directly for further details. This guide is not a recommendation to raise capital from investors, US-based or otherwise. If you need advice for your business, you are welcome to contact us for a referral.

Thanks for your thoughts! I think you got it. The trick for me is how to sift through a million sources to try and find those smaller and mid market opportunities early! But we’re working on it… :)