February 2026: Canadian Mid‑Market Financings and Transactions

Get benchmarks and financing ideas from these February transactions in the Canadian Mid Market.

Feb 2026 Mid-Market Transactions Overview

February 2026 was an unusually active month for Canada’s mid‑market deal scene. Our research examined financings, mergers and acquisitions (M&A) and other corporate transactions announced or closed during the month.

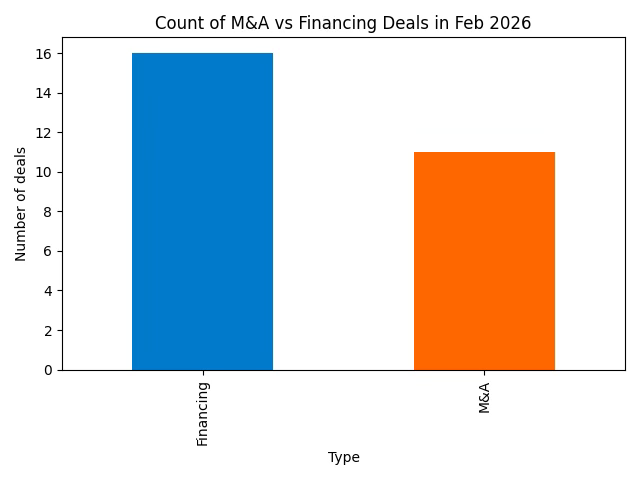

The dataset includes 27 deals spanning technology, life sciences, real estate, consumer goods and, most notably, the mining and energy‑transition sectors. Financing transactions outnumbered acquisitions (16 financings vs. 11 M&A deals), yet a handful of large M&A deals dominated the headlines.

Mining‑focused companies raised capital for exploration projects across Canada and abroad, while strategic buyers pursued acquisitions to expand capabilities in data centres, digital forensics, health technology and packaging.

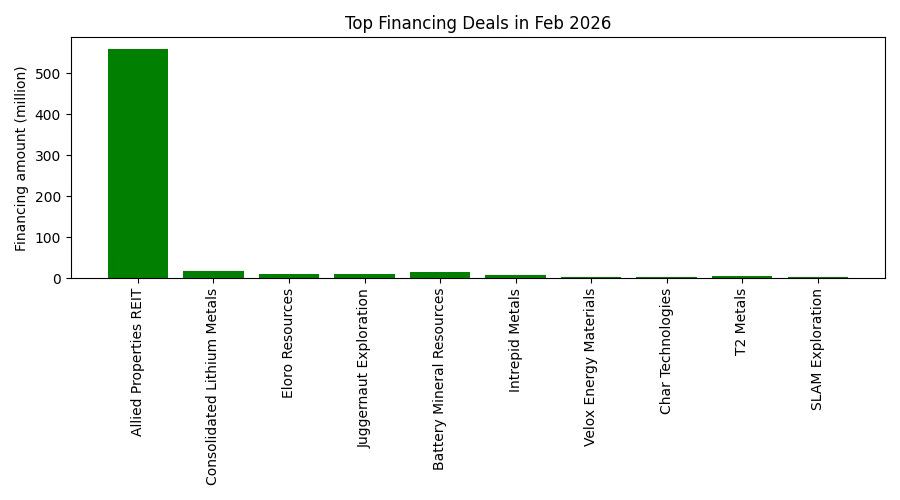

In total the financing transactions captured here raised approximately C$637 million. This total is skewed by a single $560 million offering from Allied Properties REIT; the median financing size was around C$2.9 million, illustrating how mid‑market capital raising activity tends to involve relatively small rounds.

The chart below compares the relative count of M&A and financing transactions, highlighting the greater prevalence of financings.

Key M&A Transactions in Canada (Feb 2026):

atNorth acquisition – CPP Investments & Equinix. On 27 Feb 2026 the Canada Pension Plan Investment Board (CPP Investments) and U.S. data‑centre operator Equinix jointly announced a definitive agreement to acquire atNorth, a Nordic high‑density colocation provider (source).

The transaction values atNorth at US$4 billion; CPP Investments will contribute roughly US$1.6 billion for a 60 % stake while Equinix will hold 40 %.

AtNorth operates eight data centres and has several more under construction in the Nordics.

The buyers cited strong demand for high‑density and sustainable data‑centre infrastructure, noting atNorth’s use of renewable energy and heat‑recovery systems.

GSK buys 35Pharma. London‑based pharmaceutical company GSK entered an agreement on 25 Feb to purchase 35Pharma Inc., a Montreal‑based clinical‑stage biotech company (source).

GSK will pay US$950 million in cash to acquire all outstanding shares.

The deal brings 35Pharma’s investigational drug HS235, an activin‑signalling inhibitor for pulmonary hypertension, into GSK’s pipeline.

35Pharma’s announcement emphasized that GSK is acquiring 100 % of the equity and that closing is subject to regulatory approvals (source).

Soteria Flexibles acquires Imaflex. Flexible‑packaging manufacturer Imaflex Inc. announced that on 27 Feb 2026. Soteria Flexibles AcquireCo, an affiliate of U.S. packaging firm Soteria Flexibles Corp., had completed a plan of arrangement to acquire all of Imaflex’s outstanding shares at C$2.35 per share, implying approximately C$123 million in equity value. Imaflex shareholders approved the arrangement on 19 Feb and the transaction received final court approval on 20 Feb. Following the deal, Imaflex shares will be delisted from the TSX Venture Exchange (source).

Highlander Silver–Bear Creek Mining combination. Highlander Silver Corp. and Bear Creek Mining Corporation completed a statutory plan of arrangement on 26 Feb in which Highlander Silver acquired all Bear Creek shares in exchange for 0.1175 Highlander shares per Bear Creek share.

The arrangement also involved debt‑settlement agreements; Highlander paid US$6.2 million to Royal Gold and US$1.6 million to Equinox Gold.

As a result of the transaction Bear Creek will be delisted and become a wholly‑owned subsidiary of Highlander Silver (source).

Thoma Bravo takes Dayforce private. On 4 Feb 2026, private‑equity firm Thoma Bravo completed its acquisition of Dayforce Inc., valuing the human‑capital‑management software company at US$12.3 billion (source).

Dayforce stockholders received US$70 per share in cash and the company’s shares were to be delisted from both the NYSE and Toronto Stock Exchange.

Thoma Bravo and Dayforce executives said the partnership would accelerate product innovation and growth.

WSP Global acquires TRC Companies. Engineering and professional‑services giant WSP Global closed its purchase of TRC Companies on 24 Feb. TRC adds about 8,000 professionals and strengthens WSP’s power and energy platform; the company highlighted ambitions to become the largest U.S. design and engineering firm by revenue. Financial terms were not disclosed (source).

Ricoh Canada buys ET Group. Ricoh Canada announced on 3 Feb that it had acquired ET Group, a Toronto‑based workplace‑technology integrator, expanding its digital services and collaboration solutions. ET Group will operate as a wholly‑owned subsidiary of Ricoh Canada (source).

Cellebrite to acquire SCG Canada. Digital‑forensics company Cellebrite announced on 11 Feb that it had agreed to acquire SCG Canada Inc., a provider of portable digital‑forensics solutions for drones. Cellebrite’s blog said the acquisition will broaden its capabilities in drone data collection, citing the growing importance of drone evidence in investigations (source). Deal terms were not disclosed.

Bold Ventures and other smaller acquisitions.

On 27 Feb, exploration company Bold Ventures signed a deal with Emerald Geological Services to acquire six mining claims contiguous to its Joutel property in Quebec in exchange for 750,000 common sharesboldventuresinc.com. These claims cover geophysical anomalies previously identified, and the transaction is subject to TSX Venture Exchange approval (source).

Restart Life Sciences closed its acquisition of the Holy Crap cereal brand the same day, adding over $1 million in annualized revenue and acquiring trademarks, intellectual property and a manufacturing facility (source).

WELL Health Technologies completed its acquisition of E‑Consult Canada LP and eight Alberta clinics effective 1 Feb (announced 4 Feb). WELL acquired a 61 % majority interest in the technology‑enabled e‑consult platform for approximately $33 million cash and simultaneously absorbed the clinics; the company expects the acquisition to add about $45 million in pro‑forma annual revenue (source).

Canadian Financing and Capital‑Raising Activity

Financing transactions were even more numerous than acquisitions and were heavily concentrated in the mining sector. Many issuers relied on non‑brokered or bought‑deal private placements, often using Canada’s Listed Issuer Financing Exemption (LIFE) to expedite capital raising. Proceeds were typically earmarked for exploration programs or general working capital.

Large financing rounds in February 2026:

The largest offering of the month came from Allied Properties REIT, which closed a C$560 million marketed public offering and concurrent private placement on 18 Feb. Allied issued 56 million units at $10 per unit and planned to use proceeds to repay credit lines used to refinance debentures (source).

Consolidated Lithium Metals announced on 26 Feb a non‑brokered private placement to raise up to C$17.07 million by issuing LIFE units, flow‑through shares and charity flow‑through units to fund exploration at its Kwyjibo rare‑earth and lithium properties (source).

Eloro Resources launched a bought‑deal private placement on 24 Feb selling 3.846 million shares at C$2.60 to raise C$10 million (with an option to increase by C$2 million) for the Iska Iska silver–tin project in Bolivia (source).

Juggernaut Exploration entered a bought‑deal private placement on 27 Feb with Stifel Canada to sell 3.906 million flow‑through units at $2.56, raising C$10 million to fund exploration on its Big One gold project (source).

Battery Mineral Resources announced a non‑brokered private placement to raise between $10 million and $25 million at $0.20 per share to support operations at its Punitaqui mine in Chile (source).

February 2026 | Medium‑sized placements:

Intrepid Metals closed a non‑brokered private placement on 24 Feb raising C$6.5 million; Teck Resources invested roughly C$4.1 million and will hold 19.9 % of the company (source).

SLAM Exploration initially announced on 18 Feb a $1.17 million placement and upsized it two days later to C$2.034 million, issuing 22.6 million units at $0.09 each to finance exploration on its Goodwin and other projects (source).

T2 Metals arranged a non‑brokered private placement on 27 Feb of up to 10 million units at $0.50 per unit to raise $5 million for exploration in Yukon and Manitoba (source).

Smaller Canadian financings in Feb 2026:

Several issuers raised between C$0.3 million and C$3 million:

Char Technologies announced a non‑brokered placement on 23 Feb of up to 8.511 million units at $0.235, targeting about C$2.0 million, with BMI Group agreeing to take half the offering (source).

Telo Genomics increased its convertible‑debenture placement to $1.6 millionon 27 Feb, offering 15 % debentures convertible at $0.05 and attaching two million warrants per $100k of debentures (source).

Trojan Gold launched a flow‑through private placement to raise up to C$0.3 million (source), while Canadian Silver Hunter completed a placement raising $0.5 million (source).

Velox Energy Materials proposed a placement on 27 Feb of 89.3 million units at $0.035 to raise roughly $3.125 million, noting that a director intended to participate for up to 5.7 million units (source).

Stria Lithium repriced its planned financing on 25 Feb and closed it on 26 Feb, issuing 2.127 million units at $0.47 to raise about $1 million, with each unit carrying a warrant exercisable at $0.59 for 36 months (source).

Tsodilo Resources closed a placement on 2 Feb issuing 4.947 million units at $0.15 for C$742,095 (source).

Bold Ventures’ share‑based acquisition of mining claims, although not a cash raise, was executed through the issuance of 750,000 shares.

The bar chart above illustrates the relative scale of the largest financing rounds, highlighting how Allied Properties REIT’s transaction dwarfed other deals.

Spin‑offs and Other Corporate Developments

The month also featured several plan‑of‑arrangement transactions and spin‑off‑related developments.

Highlander Silver’s purchase of Bear Creek Mining and Soteria’s acquisition of Imaflex were both structured as plans of arrangement under Canadian corporate statutes (source, source).

MTL Cannabis shareholders approved Canopy Growth Corp.’s plan to acquire their company on 17 Feb; however, the closing of that transaction was expected to occur later in March and is therefore beyond the scope of this report (source).

In the life‑sciences sector, Aptose Biosciences amended its arrangement agreement with Hanmi Pharmaceutical on 24 Feb to push its shareholder meeting to 31 March, signalling continued negotiation rather than a completed deal (source).

Trends and Analysis - Feb 2026 Mid-Market Financings

Mining drives deal volume

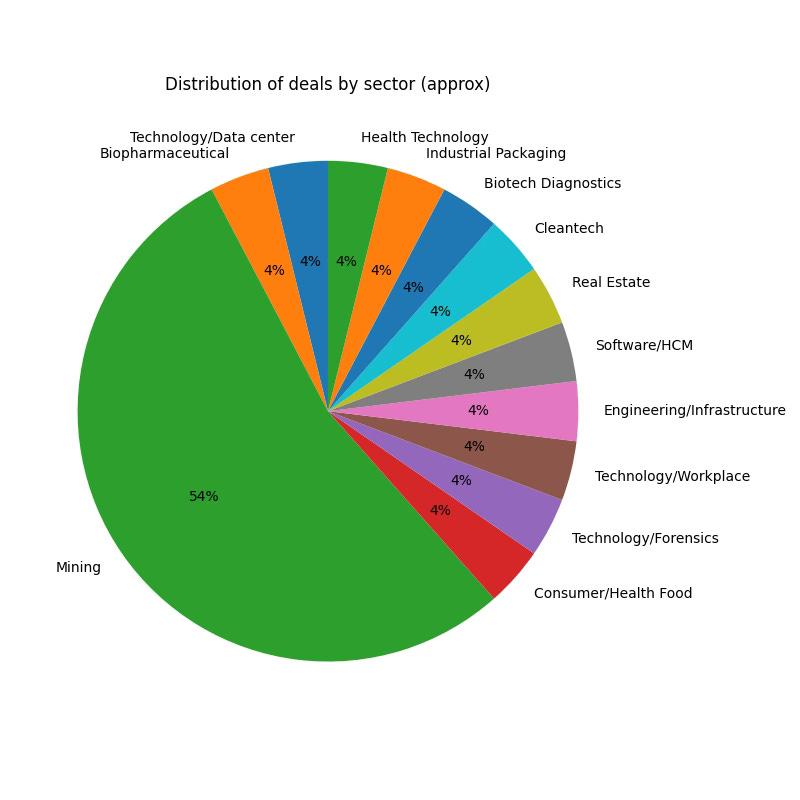

Mining and exploration companies accounted for about 54 % of the transactions observed.

These deals ranged from small C$0.3 million flow‑through placements (Trojan Gold) to multi‑million‑dollar bought deals (Juggernaut and Eloro) and a large C$17.07 million offering from Consolidated Lithium Metals.

The prevalence of mining deals reflects heightened investor interest in precious metals and critical minerals such as lithium, copper and rare earths.

Many financings were structured as flow‑through or charity flow‑through units to provide tax benefits to investors.

Concentration of capital in a few large offerings

While 16 financing transactions were recorded, the C$560 million Allied Properties REIT offering accounted for roughly 88 % of the total capital raised.

Excluding this outsized transaction, total financing for the month was around C$77 million and the average deal size dropped to ~C$5 million.

The median financing round (C$2.9 million) shows that most issuers tapped the market for modest sums, often to fund exploration programs or working capital.

Strategic M&A across diverse sectors

The M&A landscape in February 2026 was varied. Large transactions included Thoma Bravo’s US$12.3 billionDayforce deal and the US$4 billion atNorth acquisition, demonstrating ongoing appetite for platform‑scale technology assets.

Mid‑market transactions targeted niche capabilities—digital‑forensics firm SCG Canada, workplace‑technology integrator ET Group, high‑density data‑centre operator atNorth and flexible‑packaging manufacturer Imaflex—suggesting that buyers are positioning themselves for longer‑term digital transformation and supply‑chain resilience.

Life‑sciences transactions such as GSK’s purchase of 35Pharma illustrate the continuing consolidation of drug‑development pipelines.

Regulatory and shareholder approvals matter

Several transactions were contingent on court or shareholder approvals.

Imaflex’s acquisition by Soteria required a special meeting of shareholders and court approval before closing.

Similarly, Highlander Silver’s arrangement with Bear Creek Mining included debt settlements and early‑warning filings.

In the cannabis sector, MTL Cannabis shareholders overwhelmingly supported Canopy Growth’s plan of arrangement; however, closing was still subject to final court and regulatory approvals.

These examples underline the procedural complexity associated with Canadian plans of arrangement and the importance of regulatory compliance. Be aware, operators.

February 2026 Canadian Mid-Market M&A Conclusions:

Canada’s mid‑market transaction landscape in February 2026 was characterised by intense financing activity—particularly in the mining sector—and a handful of strategically significant acquisitions.

The prevalence of small flow‑through placements illustrates continued reliance on investor tax incentives to fund exploration, while the outsized Allied Properties REIT offering skewed aggregate financing statistics.

On the M&A side, buyers pursued assets that augment digital infrastructure (atNorth), expand data‑forensics capabilities (SCG Canada) or add specialised packaging and technology expertise (Imaflex, ET Group).

The successful completion of these deals signals confidence in long‑term trends such as cloud computing, digital health, sustainable packaging and the energy transition. Going forward, the interplay between commodity markets, technological disruption and regulatory processes will continue to shape Canadian dealmaking.

Risk Disclaimer and Intended Use: This report is intended to act as an educational resource, - not a definitive recommendation. Please reference underlying sources directly for further details. This report is not a recommendation to raise capital from investors, US-based or otherwise. If you need advice for your business, you are welcome to contact us for a referral

.